Moneysworth wins Best Small Protection Advice Firm 2023!

Learn more

Call us 01625 462 744

If you have a life insurance policy, you might think that the only role your insurer plays is to provide you with vital peace of mind. You pay your premium each month and, in return, the insurer keeps your policy in force, one which will provide much needed funds for your loved ones should the worst happen.

Increasingly, however, insurers are developing new ways of supporting their customers.

For example, the following support services might be on offer:

No one insurer will offer all of these, and the exact level of support varies from one provider to another, but it’s likely that your insurer will offer quite a few of these support services.

This support is very welcome indeed in the modern world, where cost of living pressures are all too obvious, and where one in four of us experience mental illness, not to mention the fact that many people struggle to get NHS GP appointments.

According to charity Mind, one in four of us every year will be affected by some form of mental health condition.

Not only are mental health problems, unfortunately, very common in today’s society, there is also undoubtedly a stigma that surrounds this issue, and this inevitably has an impact when it comes to insurance applications made by people with a history of mental health issues.

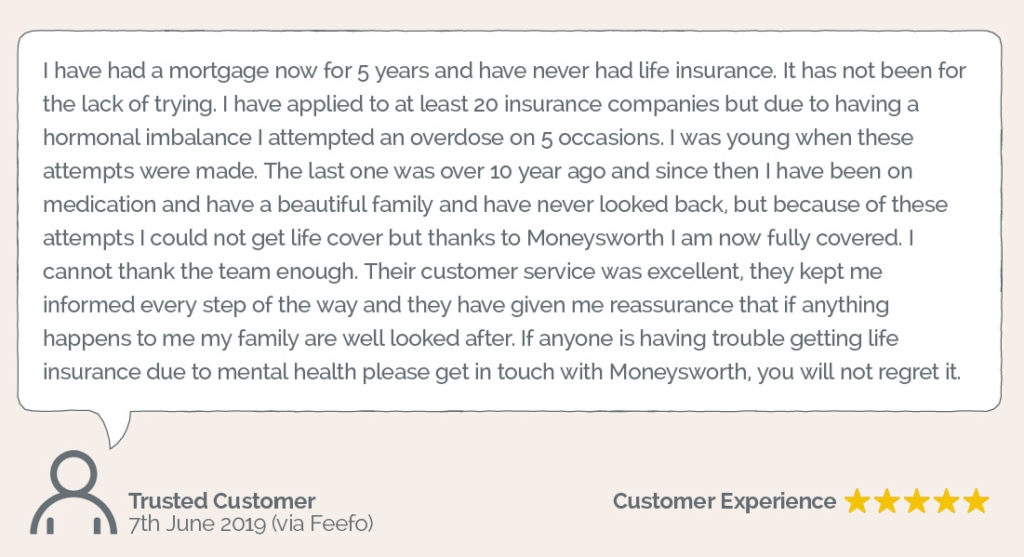

The good news is that not every insurer thinks in the same way, and Moneysworth’s previous successes demonstrate that it is certainly possible to obtain affordable life insurance if you have experienced mental health difficulties. If you have been declined by one or more insurers because of your mental health history, then give Moneysworth a call today as we have frequently been successful in obtaining policies for clients who have been declined elsewhere.

Moneysworth’s highly skilled and experienced team are experts in assisting people with both mental and physical health conditions to obtain the cover that they need.

Recent examples of where we have been able to obtain cover for clients with mental health issues include:

31-year-old woman with a history of various mental health conditions

26-year-old woman with a history of depression and other complications

33-year-old woman who had experienced both OCD and depression

50-year-old man with a history of depression and anxiety

We can help you find the right insurance if you have experienced a number of mental health conditions, which include:

Moneysworth promise to be sensitive to the individual needs of clients with mental health issues, and we promise to treat all of our clients in a compassionate manner. We allow our clients a choice of communication options and we find that many clients with mental health issues feel more comfortable doing everything via email.

For over ten years, mental health campaign Time to Change has been working to improve attitudes and behaviour towards people with mental health problems.

The movement was started by the charities Mind and Rethink Mental Illness, and their work has resulted in 12.7% of the population (5.4m people) now having more positive attitudes to mental health.

Of course there is still some way to go. The prejudices people face can mean losing jobs, relationships and in the most extreme cases, lives. Time to Change is committed to continue their campaign until people no longer hold views which make life unnecessarily harder for those affected.

We really admire this campaign, and so this year we have decided to support their ‘Time to Talk Day’. As a specialist broker which deals with many people living with mental health conditions, we understand that some people find it difficult to talk about issues which affect them when they’re looking for life cover to protect their families and homes.

Not only do we welcome the opportunity to talk to people, we also understand that some people may prefer email communication rather than talking over the phone. We’re happy to do either!

Without someone to offer expert guidance, applying for Life Cover can be stressful. We do everything we can to make the process as easy and simple as possible for you.

Since Moneysworth started in 2003, our team has helped many people with various mental health conditions to find suitable Life Insurance.

Andrew Wilkinson and Tim Boddy, Moneysworth’s founding partners, have personal experience of some of the key issues involved and comprehensive knowledge of the Life Insurance market.

We’re also aware of how, when people living with mental health conditions are refused the opportunity to protect their family’s future, those decisions often negatively impact their recovery.

A significant factor in Moneysworth winning Best Specialist Intermediary 2019 at the Cover Excellence Awards was recognition of our work for customers living with mental health conditions.

We want to see cover options and availability broaden for people living with mental health problems, and so we’ll continue to lobby the insurance industry for better outcomes for all.

We research the whole market and also offer access to alternative solutions.

We don’t charge clients any fees to search the insurance market, so it won’t cost you a penny to ask us to fully explore your Life Insurance options.

Choose your preferred option:

Our client was looking for life insurance to cover the mortgage on their family’s home. Due to the client’s mental health history (which included a significant event within the last five years), they had been declined cover by two major insurance companies.

“When I first applied for life insurance, being told by my initial advisor [name supplied] that my condition and medical history which had been caused by a hardship in my life would make it both difficult for me to obtain life insurance, and could potentially mean I can’t obtain life insurance was a real scare for me, and made me feel guilty for going through what I had gone through and trying to seek help during a tough period in my life. A period where I should have been excited and overjoyed buying a house with my partner was overlooked by more anxiety and worry that I wouldn’t be able to obtain life insurance to make sure the mortgage for my partner was sorted if I were to pass (which frankly I find really unfair).”

Feedback received from the client (June 2019)

The client approached Moneysworth for assistance. We spoke with the client about the details of their mental health history. Then we contacted underwriters at insurance companies across the market to ask how they might react if the client were to make an application to them. Some insurers stated that they would decline an application but others said they might consider offering the requested cover but at a cost of around 10 to 15 times greater than the normal standard premium rate (the monthly fee to be paid by the client for their insurance).

We explained to the client that the reason for the high premiums was due to the risk of suicide, based on their mental health history.

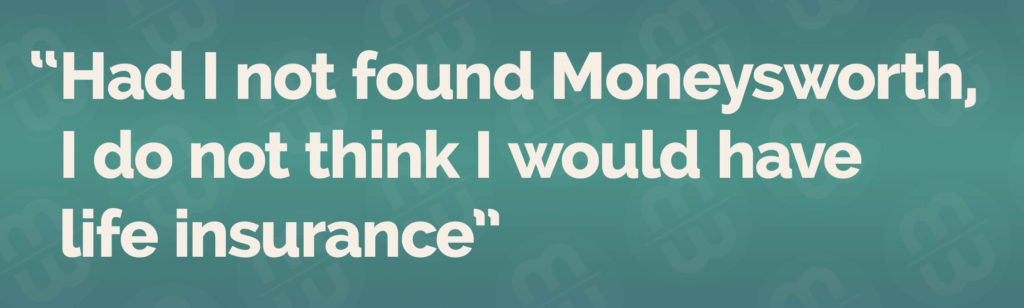

“After doing extensive research online, upon finding Moneysworth, they were one of the very last options for me, so after giving them a ring and discussing my situation, it was somewhat reassuring that I felt like I was not alone, and unlike my previous advisor they had my back. Had I of not found Moneysworth, I do not think I would have life insurance. I was told by someone on the phone from one insurance company [name supplied] to ‘not bother for around 5 years’.”

Feedback received from the client (June 2019)

We mentioned to the client that the Moneysworth team has been very concerned about outcomes like this. We’re aware of many cases of people in similar situations, in which insurers have declined to offer any Life Cover, or have told clients to come back to them in several years if their mental health circumstances improve.

“The thought of having to pay 10-15 times the normal premium for life insurance as a first time buyer with all my other bills to worry about felt unfair, as I have mentioned above. I don’t drink (expect for very special occasions), I don’t smoke, I stay fit and physically healthy. It felt like insurance companies were manipulating a hardship in my life that really took its toll on me and that I did not want to be reminded of. I didn’t do what I did in the past for the sake of it, it was a genuine time in my life where I struggled, and I think that insurance companies are failing to recognise this.”

Feedback received from the client (June 2019)

We also explained that, at the time, Moneysworth had recently begun a trial scheme with a mainstream insurance company Royal London, which aimed to give such clients the possibility of obtaining the Life insurance they were seeking with a premium which clients would deem to be significantly more affordable. This new Life Cover option achieves this by excluding self-inflicted death for the term of the policy. The client was willing to accept this exclusion, and decided they would like to apply.

We made the application to Royal London with the client. The insurer contacted the client’s GP for a medical report. They then made the decision to offer life insurance.

The client obtained nearly £170,000 of life cover for a term of 30 years for a guaranteed premium for the whole term of just under £9 per month. The policy covers them for death from all causes, with the exception of suicide.

We asked the client what they would have done if this new alternative type of cover had not been available. Would they have wanted to apply for life insurance that cost an estimated 10 to 15 times more than someone with a clean bill of mental and physical health? The client told us that because they had death in service benefit from their employer, they wouldn’t have applied.

We then asked the client would they have applied if they did not have any death in service cover from their employer (the majority of people in the UK do not have death in service benefit from their employer). The client replied that, reluctantly, they would have felt that they had no other choice but to pay the very high premiums that some other insurers had indicated.

“Getting life insurance was so important to me, as I want my partner to be financially stable if I were to pass, even though I have a death in service benefit at work, the mortgage would take a large chunk of money from this, and there are other things that the money would need to go towards upon my death, and as such, a specific life insurance for my mortgage was really important. When Moneysworth told me I could get normal terms with the exclusion placed in, I was delighted, I know now how to deal with any struggles I have, and have been provided with the tools to combat my down moments by therapists. Ultimately it gave me the peace of mind I was searching for, and I’m not sure why this arrangement has not been adopted by insurance companies sooner, knowing how I felt and the situation I was in, I hate to think how they have made others with struggles feel, especially those who have been in a worse situation than me.”

Feedback received from the client (June 2019)

If you have had a significant mental health event within the past five years, your search for Life Cover is most likely going to be harder.

This is why asking an expert to shop around for you is a good idea. Moneysworth have over fifteen years of success in finding cover for people with mental and physical health conditions.

We don’t charge clients any fees to search the insurance market, so it won’t cost you a penny to ask us to fully explore your Life Insurance options.

You could now be eligible for a new type of Life Cover to help protect your family’s financial future.

Today is World Mental Health Day – a time to consider how mental health problems such as anxiety and depression could affect anyone at some point in their lives. It’s also a time to reflect on the social stigma that often surrounds severe mental health problems.

The statistics for mental health in the UK are alarming. Around 1 in 4 of people experience a mental health problem each year. At least 1 in 5 people have had suicidal thoughts in their lifetime. Around 1 in 15 people have self-harmed or attempted to take their own life. *

This year’s theme for World Mental Health Day is suicide prevention.

Just like anyone else, people suffering with a severe mental illness want to do what they can to protect their loved ones’ future, such as obtaining Life Insurance.

Until recently, the chances of being offered cover would have depended on the specific details of their circumstances, such as how many suicide attempts there have been, and how long ago they occurred. Even today, this is the situation with most (but not all) insurers.

UK insurer Royal London has created a new Life Insurance option that’s been specifically designed for individuals with severe mental health conditions who would otherwise be declined cover.

This new option is available to many people who have had a significant mental health event in the last five years (such as suicide attempt, suicidal thoughts, self-harm, or in-patient treatment at a psychiatric ward). It’s also typically available at a more affordable price.

Moneysworth has helped many people with different mental health problems to find suitable Life Insurance. This is because we’re well placed to help people in this situation. We have personal experience of some of the key issues involved and detailed knowledge of the Life Insurance market.

We help to ensure all relevant medical evidence for each applicant is presented as a comprehensive case to the insurer. This evidence is assessed by a specialist group of underwriters at Royal London, which helps to avoid mild conditions being classed as a higher risk.

As a result of this trial, Royal London has been able to offer cover to 75% of applicants who would otherwise have been deemed uninsurable.

“The response from customers and advisers has been overwhelmingly positive and we’ve seen high take up rates for cover despite the underwriting process being longer.”

Craig Paterson, underwriting and claims philosophy manager at Royal London

Here is a review of our service by one of the many clients we’ve helped to find cover this year:

If you have other health conditions, or have had a significant mental health event within the past five years, your search for cover is mostly likely going to be harder.

This is why asking an expert to shop around for you is a good idea. Moneysworth have over fifteen years of success in finding cover for people with mental and physical health conditions

We don’t charge clients any fees to search the insurance market, so it won’t cost you a penny to ask us to fully explore your Life Insurance options.

* Statistics source: Mind

https://www.mind.org.uk/information-support/types-of-mental-health-problems/statistics-and-facts-about-mental-health/how-common-are-mental-health-problems/