Moneysworth wins Best Small Protection Advice Firm 2023!

Learn more

Call us 01625 462 744

There’s no denying the fact that if you have a Body Mass Index (BMI) of more than, say 30, it gets harder to obtain life insurance. At this level, you are considered to be ‘medically obese’, and not only might you have to pay a higher premium, but some insurers might automatically reject your application should you apply to them directly.

Your BMI number – your weight in kilograms divided by the square of your height in metres – is an important consideration for life insurers when deciding whether to offer cover and at what price. They will, however, also consider other factors, such as your age, your personal medical history and the medical history of your close relatives.

The solution here might be to approach a specialist broker such as Moneysworth. We specialise in finding life insurance for clients whose circumstances are a little different – perhaps because they reside overseas, have a riskier occupation or have a mental or physical health concern. We have an extensive knowledge of the criteria used by different insurers and can identify the provider who will offer you the most suitable cover. For example, not all insurers have the same ‘maximum BMI’, so if one provider tells you your BMI is too high, we can approach another insurer on your behalf.

On 2nd August 2023, we were endorsed in the national press (the Daily Mail) as an example of a specialist broker who can assist in situations such as this. Alan Lakey, director at Highclere Financial Services, and a respected name in the life insurance sector, listed us as one of three specialist companies who can assist clients with high BMI and with other health issues.

When we look at 15 life insurance companies used by Moneysworth, we see that:

It’s also important to consider the BMI level that would prompt an insurer to increase your premium. Again, the precise threshold varies between different providers, but most will require you to pay more if your BMI is 32 or above, and some will ‘load’ your premium for a BMI as low as 29.

It’s very difficult for the average consumer to gain a detailed understanding of individual insurers’ criteria. If you have a high BMI, your best option is to make use of a specialist broker such as Moneysworth. We can use our detailed knowledge of insurers’ criteria to find you the very best price available, by approaching the insurers who are likely to consider your application favourably.

Here, it was immediately apparent that a number of insurers were prepared to offer cover to both clients. Where Moneysworth’s specialist knowledge benefitted the clients was that we knew exactly by how much each insurer would increase the premium. Had the clients simply searched a price comparison website and applied to what appeared to be the cheapest provider, this provider may no longer have been the cheapest option once their final offer of terms had been made.

In this case, both partners took out £113,000 of cover over 40 years. The female client’s premium was £12.58 per month, while the male client needs to pay just £9.04.

Then, as a more extreme example of how we can help:

After researching their situation, we told them that while most insurance companies would still say no, we believed we had found a company who might say yes. The insurance company wrote to the client’s GP for a report and the client also attended a brief medical screening. The insurance company was happy with the results and made a definite offer of cover, which the client was happy to accept, of £56,075 decreasing life cover over 20 years for £50 per month.

If you have approached insurers directly and been declined, or have been told by another broker that you can’t get life insurance due to your BMI or any other health issue, then contact Moneysworth today to see how we can help.

Here at Moneysworth, we’re big fans of signposting. What do we mean by that?

For an insurance provider, it’s about considering consumers’ needs – even if that insurer cannot accommodate the special needs that an increasing number of consumers have.

For example, what happens when a consumer is shopping around for life insurance and they are refused cover because they have a health condition which makes them a higher risk for insurance? This can, often incorrectly, cause consumers to think that they’re uninsurable and to give up looking for cover.

Consumers with health conditions rely on charities for information and guidance to help them overcome the complexities they face, including the difficulties of searching for suitable insurance cover.

The British Heart Foundation (BHF) is the UK’s leading charity for funding research into heart and circulatory diseases and their risk factors. For several years, Moneysworth and other specialist brokers have been listed [1] on the BHF’s website or in its guidance publications. We don’t always know how people find us, but we do know from our conversations with clients that many people come to us after contacting the British Heart Foundation. This is signposting in action!

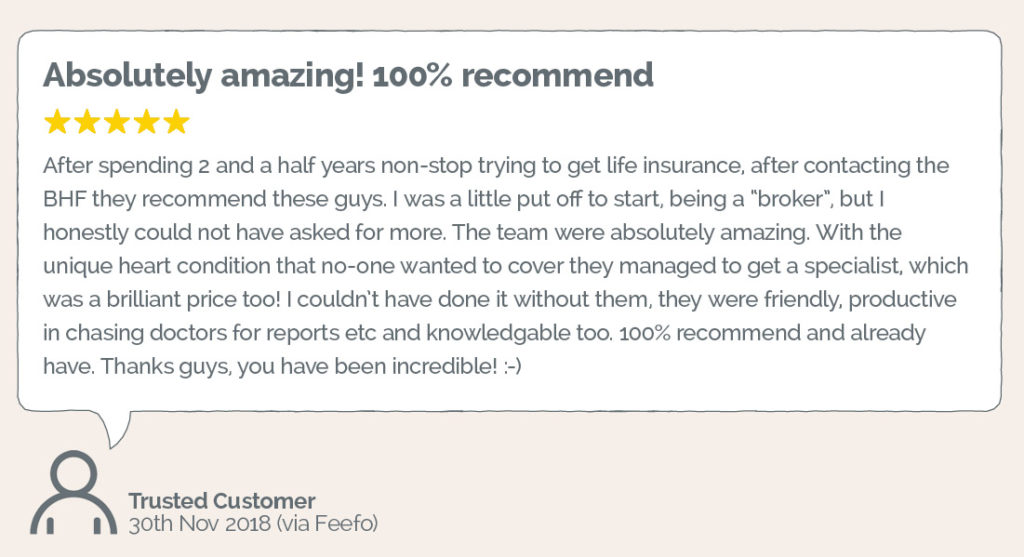

The review shown at the top of this article was written by a male client in his late twenties who was determined to protect his family’s financial future.

The problem was that, because of his heart condition, he couldn’t find an insurer who would offer him Life Cover. Soon after being born, he’d been diagnosed with a bicuspid aortic valve and coarctation of the aorta. When he was a teenager, he had open heart surgery, followed by a week in hospital and six months recuperation before returning to school.

Ever since then, he’s had annual checks at a hospital, but has no symptoms and doesn’t even need to take medication. He has no other health issues and no family history of heart defects or heart disease. He is able to work in a physical role and has an active lifestyle. Indeed, the reason he has a mortgage is because he has a steady job and income!

Yet every insurer he contacted declined to offer him Life Cover because of his medical history of having a rare heart condition.

After years of unsuccessfully searching for an insurer who would offer him suitable cover, he was signposted to Moneysworth via the British Heart Foundation.

With our specialist knowledge of the insurance market, combined with our medical knowledge, we were able to help the client find the cover he needed to protect his family’s financial future. He successfully applied for and started a Decreasing Life Insurance policy for almost £400,000 to cover a repayment mortgage over 35 years, for just under £50 per month.

Thanks to the British Heart Foundation making the effort to provide appropriate guidance and signposting, many people with heart conditions are able to find Life Cover after they’ve been declined by mainstream insurers.

Notes:

Having type 1 or type 2 diabetes often makes it harder or even impossible to find suitable Life Cover, Critical Illness Cover and Income Protection.

Life insurance companies typically have a range of different premium rates for people with diabetes. Different companies will place the same person in different price bands. The process of applying for cover can often take weeks – or even months – if medical reports need to be obtained and checked. And although the situation has somewhat improved for Life Cover in recent years, most insurers are still unwilling to consider Critical Illness or Income Protection for people with any type of diabetes.

Well, there’s definitely some good news here.

In recent years, we’ve seen improvements in the prices for Life Cover typically offered to people with diabetes.

Another encouraging development we’ve seen with a couple of insurers: after starting the life insurance policy, the insurers reward policyholders by reducing premiums if the customer can demonstrate improved control (i.e. if their HbA1c reading comes down by a certain amount). We think this is a very encouraging sign, not just because it can make cover cheaper, but because it demonstrates that the insurance market is starting to consider how to adapt to the unique circumstances of people with long-term health conditions.

If certain criteria are met, it’s now possible for people living with diabetes to get a “fast-track” application, which means cover could be in place immediately. Less stress, more peace of mind – exactly the kind of innovation we want to see for people with long-term health conditions who want to protect their financial security and their family’s future.

A year ago, there were hardly any options for people with diabetes to obtain Income Protection Insurance. For most it simply wasn’t available.

Moneysworth campaigned to improve that situation, and we’re pleased to see at least some people in the insurance industry listened to us!

With expert guidance, it’s now possible for some people who have type 2 diabetes to get Income Protection with no exclusions, subject to certain criteria. But for people with type 1 diabetes, although there is some availability, it’s extremely limited.

The situation for Critical Illness Cover has been slow to improve. It is now possible for people living with diabetes to obtain Critical Illness Cover – but the options are very limited and the chances of being offered cover are even narrower if they have type 1.

The small signs of progress we’ve seen in the market are a welcome start, but the fact is most insurance companies still don’t offer either of these protection products to people who have diabetes.

The charity Diabetes UK reports that there are around 3.7 million people who have been diagnosed with diabetes in the UK, and that figure is predicted to rise to 5 million by 2025*.

In light of this, we firmly believe that the insurance market needs a surge of innovation to make its products and services more forward-thinking and inclusive.

Moneysworth wants to see cover options and availability broaden for people living with diabetes, and so we’ll continue to lobby the insurance industry.

* Source: Diabetes UK ‘Facts & Figures‘

I have been trying to get my ahead around some statistics that I came across yesterday.

Sainsbury’s commissioned the research looking at how many people in the UK had mortgages with no life cover in place to repay the outstanding balance. The results show some surprisingly big numbers, much bigger than most would perhaps guess.

Firstly the total figure of mortgages without life cover is given at £245,000,000,000 – thats a quarter of a trillion. But ‘billions’ and ‘trillions’ are everyday newspeak terms now, over used by both politicians and news reporters these words have become a sort of TV litter which we therefore tend to ignore as part of the familiar landscape.

Dig a bit deeper into the Sainsbury report figures though and we start to find more meaningful statistics.

The number of people with no life insurance to cover their mortgages? Just under 7 Million, or to put in a more meaningful way that equals just over 4 in every 10 mortgages. The report goes on to break down this figure between different age bands, as follows

Age Percentage of mortgage holders unprotected

18-24 62%

25-34 38%

35-44 33%

45-54 30%

55-64 55%

65+ 58%

Of course within these figures there will be mortgage holders who have valid reasons for not having life cover. The biggest such group will be single people with no dependants – fair enough. Another group might those with significant personal wealth.

But what about all the others? What about the significant majority who are not particularly wealthy but who do have dependent partners and/or families? What about the growing number of older people who find themselves with mortgages much later in life than they had originally anticipated? What are the reasons why these mortgage holders choose to have no life cover?

Here are some of the common reasons people give when asked.

”I’ve never really thought about it.” –

”Its a waste of money – its (my death) will probably never happen ”

”Its too expensive – I can’t afford it”

”No one will insure me with my health conditions”

But for the moment I should mention one other factor which I suspect lurks in the background for many and that is fear. Fear is a great inhibitor in all aspects of life. Fear changes our behaviour, it makes us more cautious, it makes us avoid action, fear makes us hide.

Generally people tend to fear the unknown. I am not a professional psychologist but based on my own observations fear is especially to do with a future outcome that is not known. Often the reason why people don’t face up to their fears is because they are scared as to what the outcome might be if they do. By avoiding action we feel like we are keeping the possible undesired future outcome at bay. Mostly its a subconcious kind of response.

So how does ‘fear’ apply to this issue of life cover for mortgages?

Perhaps underneath these figures many people are frightened about the questions they may be asked if they do apply for life cover. Perhaps they are frightened of having to reveal ’embarassing’ personal medical information about themselves.

Or perhaps they fear the final outcome – the fear that if they apply they they might get turned down and all that that might mean. For example it could confirm their own worst fears that they are going to die sooner rather than later, or in some way mark their financial credit record making it more difficult for them to borrow money in the future if they applied for a loan or mortgage. So some people might choose to avoid applying for life cover in order to avoid some sort of final judgement which they fear might finally mark their cards for good.

But of course fearing something does not mean that it is going to happen.

The problem is that many people are needlessly putting their families at risk by continuing to take no action. Put bluntly if you have no life cover for your mortgage on your family home then your home is at risk. If you have a family you owe it to your family to seek the appropriate life insurance in order to protect the family home for them.

Of course this for many will involve confronting a fear of the unknown.

But if only people with such fears knew where to look they might be quite surprised at the outcome. Here at www.moneysworth.co.uk we offer a specialist service for people with pre existing health conditions who are seeking life cover, for mortgages or for family protection (for other reasons too). Our service is confidential and non judgemental. We have over a number of years developed and refined a process which is designed to help customers find best outcomes. Each case is indivually researched. Further more our service is fee free to our customers and is with no obligation. Therefore it costs nothing to try.

The results are very encouraging. It should be said that we are not able to offer all customers a 100% guarantee that we will be able to find the life cover that they seek but we are able to help the majority, many of whom have been turned down elsewhere before coming to us. Very often the premiums acheived are considerably less than the customer originally feared.

Customers frequently express a high level of satisfaction with our service and often say that a great weight has been lifted for them. With the peace of mind knowing that their dependants are now protected they no longer need to live in fear.

A client recently came to us with a difficult case – subaortic stenosis.

At Moneysworth we do our best to help everyone who comes to us with a health condition to obtain life cover. We deal with a lot of heart related medical conditions, especially heart attacks, angina and heart by passes. However there are of course a number of other heart conditions, including subaortic stenosis.

Like so many who come to us this client was seeking life insurance to cover his mortgage so that the remaining mortgage debt would be cleared in the event of his death, thereby providing him and his family with peace of mind knowing that should the worst happen the family would still have thier home. In this case our client was therefore seeking approximately £150,000 life cover for a 25 year repayment mortgage.

So what made this case difficult? Unfortunately for him, our client was diagnosed in early childhood with his heart condition. Later on in his childhood our client had a surgical proceedure, which could be argued to have been mostly a success, though some some slight leakage was detected for a while after the operation. Over time the leakage appeared to stop and the client now lives a normal life.

We approached a number of insurance companies on behalf of our client who were generally reluctant to agree to provide life insurance. There were no other significant health conditions in this case and clearly most life companies remained nervous about the key underlying health condition – subaortic stenosis. Despite most life companies declining to offer the life insurance we persisted with our search. We know from experience that it does not always follow that every life company will view the same information in the same way and sometimes we have to pass by a number of closed doors before we find one that is open.

Which is exactly what happened in this case. We managed to find a life company who were willing to look at the case differently. After obtaining detailed medical information they were able to view the outcome of the operation more favourably. Whilst they wished to charge a small additional amount to reflect some additional risk, they did not regard the additional health risk factors to be significant enough to warrant declining our client’s application.

So the hard work and patience payed off and in the end we were able to acheive a very positive outcome for our client. Not only were we able to find the total amount of cover that our client was seeking, but we were able to do so at a very attractive premium of less than £17pm.

What a great result!