Moneysworth wins Best Small Protection Advice Firm 2023!

Learn more

Call us 01625 462 744

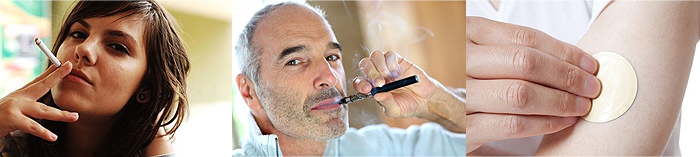

At this time of year, many people are sticking to their New Year’s resolutions and, for some, giving up smoking is one of the biggest challenges. Quitting smoking is beneficial to your health, but how does it affect your Life Insurance?

1. Smokers pay higher premiums than non-smokers – but how much higher?

For a new life insurance policy, a 30-year-old can typically expect to pay 66% more, a 45-year-old 112% more and a 60-year-old 136% more. Proof (if proof were needed) that smoking is not good for your health or your wealth! For further information on the Health Risks Of Smoking (NHS).

2. What about ex-smokers taking out a new Life Insurance policy – how are they dealt with?

Broadly speaking, it will depend on how long ago the applicant gave up smoking. For a life insurance company to charge a non-smoker rates, the period since last smoking needs to be least 12 months. ‘Non-smoking’ in life insurance company terms means no use of any tobacco or nicotine products for 12 months, which even includes E-cigarettes, patches or gums.

A ‘social smoker’ or occasional smoker is still classed as a smoker – and charged as a smoker!

3. Can insurance companies test for smoking?

Yes. The test used is called a cotinine test and a life insurance company can request such a test as part of their assessment process for a life insurance application.

Indeed, if the insurer requires you to attend a nurse screening or medical exam as part of the process, and you’ve told them you’re a non-smoker, they will test you at that time anyway. In addition to this, many peoples’ GP medical records contain information about their smoking habits.

4. What if someone is now an ex-smoker, but they have an existing Life Insurance policy taken out while they were still a smoker?

There may be the potential to get a lower premium rate – but it won’t happen automatically, and you will need to take action in order to explore this potential option. Some companies will, if requested, be prepared to alter the premium on your existing plan from smoker to non-smoker rates, once they have satisfied themselves of your non-smoking status (12 months non-smoking – and expect to be asked to do a cotinine test).

However, the majority of insurance companies will not be prepared to change your existing policy terms and therefore in order to obtain non-smoker premium rates you will need to make a fresh application. It is very important that if you do make a new application that you do not cancel your existing policy until the new policy has started. This is because a new application means a fresh assessment, taking into account your age (obviously you will be older) and any changes in your health. Remember that, for some people, these factors could make the final ‘non-smoker’ premium for the new application more expensive than the old policy ‘smoker’ premium rate. Indeed, in a few cases, health changes might be so significant that a new policy is not available.

5. If someone is thinking about giving up smoking – is it best for them to wait until they become a non-smoker before applying for life insurance?

No. Waiting is a big mistake and could cost you dearly! Nobody likes paying more than they need to and you might be tempted to wait until premiums become cheaper.

But there are a number of risks with this approach:

Firstly, and most importantly, waiting until you qualify for non smoker premium rates leaves your loved ones with no cover and still fully exposed to the financial consequences of you dying before you complete the qualifying conditions for non-smoker premium rates.

Secondly, changes to your health might occur before qualifying for non smoker premium rates, which could mean that the cost of cover actually increases and, in the worst cases, becomes unavailable – which could amount to a potential disaster.

Thirdly, as a smoker today you don’t know how long in reality it may take you to complete a full continuous period 12 months of non-smoking. When will you quit? How long will you use nicotine substitutes? Will you have an occasional cigarette? For some, despite their good intentions, they may never reach a point where they have not smoked or used any nicotine replacement products for 12 months.

If higher premium rates for smoking are a real concern then rather than doing nothing it is better to consider taking out a lower amount of cover now, with a view to reviewing the amount of cover as and when non smoker premium rates become available.

Tips for smokers applying for Life Insurance:

It’s worth also remembering that the potential longer term consequences of smoking involve a greater risk of certain health conditions, several of which (such as heart attack, lung cancer, other cancers, stroke, etc.) are potentially claimable conditions for Critical Illness insurance policies.

What is generally not realised nor fully understood is that millions of people in the UK are unable to obtain a Critical Illness policy due to an existing health condition. We tend to pick up health conditions as we age and smoking increases the risk of certain health conditions. So, for smokers, it might well be a good idea to consider taking out Critical Illness Insurance sooner rather than later – especially for younger smokers, for whom premium rates are often significantly lower compared to older smokers.

A tricky shareholder protection case involving an older director with a serious heart condition and a healthy younger director, requiring careful consideration, knowledge and planning to reach a good workable final solution, while being careful to avoid a few banana skins on the way.

When our client approached us to help him find £500,000 life insurance, both he and we knew that it wouldn’t be easy. Aged 55 our client had severe artery disease, sufficient to have required a total of six stents to be fitted over a three year period. The client wanted to ensure that if he died his wife would receive £500,000 and that his 50/50 business partner would be left with 100% of the business.

We began by further researching the client’s medical profile and potentially available options with insurance company underwriters. A specialist insurer suggested they might be able to consider offering terms at an indicative premium of £1182pm, but we felt we could do better! Medical underwriting requirements included full GP reports with cardiologist letters and a medical examination. When final underwriting results came through we had managed to obtain terms at a premium of £365pm. Brilliant!

However the job was still not finished.

A further issue related to the valuation of the business which it turned out was worth significantly less than the amount our client wished his spouse to receive in the event of his death. We explained that there was a straight forward solution to this problem. Rather than conflate the need for a sufficient amount of death benefit for his spouse with the requirement to ensure that he and his business partner received each others shares in the event of death, we suggested he first take out a shareholder protection policy based on a fair and justifiable business valuation. The realistic business valuation given was £200,000 so we suggested a policy for £100,000.

Secondly we suggested he take out a separate life insurance plan for the benefit of his spouse as a Relevant Life Plan. Not only would he effectively pick up tax relief on the lion’s share of the total protection premiums but it also helped to significantly reduce the impact that ‘premium equalisation’ for shareholder protection would otherwise have had on his business partner, who of course would be liable for personal income tax on our client’s shareholder protection life insurance premiums paid for by the business. This was especially significant given that the premiums for his cover were 770% of the cost the premiums for his fellow shareholder, due to his business partner being significantly younger and with no rateable health conditions.

We also gave the client the option (which he took) of further increasing his total life cover by a further £100,000 bearing in mind how difficult it might be to obtain more cover in the future should his health change, as £600,000 was the maximum level the insurer could offer without the need for any further medical evidence.

We arranged the necessary policies for both him and his business partner (£100,000 shareholder cover and £500,000 relevant life cover each) and assisted our clients with the necessary trust documentation for all the policies, making sure that in the event of a claim the right amount of cover ended up in the right place quickly and without any further tax liability. We also provided them with a draft life company double option agreement for them to share with their lawyer.

Hello and Welcome!

We are proud to launch our new website which with a great deal of consideration, has taken over a year to develop.

The new site is very different to the old one and we thought it might be useful to explain some of the thinking that has gone into the design and content.

Firstly we were aware that our website had not kept pace with the changes in our business and especially our client groups. Put simply any visitor to the old site might well conclude that our life cover services were designed only for people with pre existing health conditions. However the truth is that we arrange life cover for a much wider range of clients, including people with no health conditions, business owners and clients with occupational and/or overseas travel issues.

Secondly we knew that the old website looked dated and the new site needed a much fresher approach. Financial services websites generally are often criticised for being somewhat dull, so it was important to us that visitors find the new site visually stimulating and engaging.

Our clients receive a bespoke personal service and we wanted the new website to visually send a clear message to visitors, that we are different. We have tried hard to make the site easy to read and visually engaging by breaking information down into manageable amounts. We have used space to de-clutter and chosen a font which feels personable (and different again) and is easier on the eye.

Functionality was another key consideration. We have tried to make the new website easy to navigate and as simple to use as possible. We have tried to make it easy for customers to communicate with us, whether making an enquiry or asking us any questions (e.g. email, phone, live chat). It’s really easy for visitors to share a link to any page they think may be of interest with a friend. Underlying all of this is a clear invitation for visitors to engage with us.

Finally we wanted to create a website that visitors find genuinely useful and compelling. In short we want people to leave our site feeling their visit has been worthwhile and the key issue here is the quality of the content.

Here we have tried as much as possible to put ourselves in the shoes of our clients. We asked ourselves time and time again ‘what are the questions that customers really want answers to?’ ‘How are customers feeling as they approach applying for life insurance?’ ‘What concerns do they have?’ ‘What information might help customers feel more confident’? For example, some people with pre-existing health conditions may fear that life insurance premium rates would be completely unaffordable in their particular situation. They may fear the embarrassment explaining that it was unaffordable. For some these potential negative outcomes might cause them to avoid making any enquiry at all. It is for this reason that we have decided to include a selection of real cases, showing actual premium and cover amounts achieved for some of our customers on the diabetes and heart condition pages of the site. Throughout the website we have similarly tried to include lots of additional information which we think visitors might find useful.

When it comes to life insurance, we believe that what customers are looking for above all, is to feel confident in the decisions they are making. We hope you find our website of genuine value and we look forward to being of service.

The latest Scottish Provident set of claims statistics make for some interesting reading – there are both positive and negative points.

The £43 million in claims paid in the first half of the year is not an insignificant sum and the total now stands at over £1 Billion in critical ilness payouts since 1996. Thats a huge sum of money which will have benefited alarge number of people in their hour of need and proves what a valuable social function life companies perform.

Reading the more detailed report information provides a valuable insight., for example the average period from start to claim is 9 years and the average age at claim is 49.

The critical illnesses producing the highest amount of claims are Cancer 60%, Heart Attack 16% and Stroke 6% and the report further breaks down the cancer claims showing the biggest claim areas as breast 34%, bowel/colon 11%. malignant melanoma and prostrate both at 7%.

But….. the report shows that 7% of claims were not paid and this remains a concern. The two reasons given are a) material non discloure at the point of application and b) not meeting plan definitions and the report provides some examples of each.

Non-Disclosure – There will always be a small number of applicants who deliberately withold relevant medical information and if they are intent upon doing so there then this is their responsibility alone and this is a point which should be acknowledged by those who are critical of the life insurance companies.

However we need to ask ourselves whether as an industry we are really doing all we can to try and avoid ‘non deliberate’ non disclosure. Furthermore we would do well to consider whether this is always a point of sale issue. It is a fair question to ask how much non disclosure might be resulting from the fast track underwriting process itself. Are we sure that the right messages are being sent out if we are asking only a limited number of questions or where we are asking questions which refer to certain health events only within the last five years?

Interestingly a significant percentage of clients with pre existing health conditions express to us their preference for an underwriting process which includes the obtaining of medical evidence from their GP. They feel that this might cover anything they accidentally failed to remember.

What really would be of value would be to see insurance companies publishing comparisons between the rates of non disclosure applying to cases underwritten 1) without and 2) with further medical evidence.

Not Meeting Claims Definitions – This remains a thorn in the side of the life industry and we need to consider whether there is not room for improvement in how this issue is being dealt with. What we have at the moment is a stand off between the life insurance industry who claim that they are comitted to paying all ‘valid’ claims and those who claim that the industry deliberately rejects some claims that should be ‘valid’.

But in a standoff not much progress is made.

What needs to happen is for both sides to sit down with each other and work together. The long term prospects for the sales of critical illness and other socially valuable protection policies would benefit considerably from involving the consumer in the design, decision making and marketing process. The same applies to a number of other issues currently affecting the life insurance industry (eg STIP, simplified products, activities of daily living, consumer education).

There is a fear among many consumers of non payment at claim. This fear is sufficient to stop some from buying and for some it provides a convenient excuse not to buy. But even among many of those who do buy there remains a nagging doubt that the insurance they have purchased will turn out to be ‘invalid’.

A great deal more needs to be done to research this problem.

It also highlighted the importance of having a comprehensive will to protect your wishes.

It also highlighted the importance of having a comprehensive will to protect your wishes.