Moneysworth wins Best Small Protection Advice Firm 2023!

Learn more

Call us 01625 462 744

The British Heart Foundation says that 7.6 million people in the UK are living with some form of heart condition. Whilst there are still unfortunately a number of deaths from heart-related issues, deaths due to heart issues are falling.

So what does this mean for people with a heart condition who want to take out life insurance?

An insurer is likely to regard your heart condition as an additional risk factor when assessing an application. The good news, however, is that there are insurance companies who will consider people with heart issues. There are clear benefits though to arranging your life insurance with a specialist broker such as Moneysworth.

If you have been declined by one or more insurers because of your previous heart trouble, or you have been told by another broker that your health issues mean you cannot get life insurance, then contact Moneysworth today. We have often been successful in obtaining policies for clients who have been declined elsewhere.

Having a heart condition need not necessarily mean that you have experienced a heart attack in the past. We can also assist clients who have experienced:

Moneysworth’s highly skilled and experienced team are experts in assisting people with many different mental and physical health conditions to obtain the cover that they need.

Recent examples of where we have been able to obtain cover for clients with heart issues include:

58-year-old man who had experienced a heart attack

29-year-old woman with transposed arteries and stenosis

47-year-old man with Essential Thrombosytheria

33-year-old woman who had undergone a valve replacement

44-year-old man who had undergone surgery on two occasions

These cases illustrate that it can still be possible to obtain life insurance where:

If you would like to find out more, then contact Moneysworth today!

In our previous article, we gave an example of how charity signposting works. A young father with a lifelong heart condition tried for over two years to find an insurer willing to offer him Life Cover. Then a UK heart charity providing him with a list of brokers who specialise in assisting people with health conditions to find suitable insurance.

Likewise, a growing number of financial advisors now signpost to us when they have clients whose health condition is deemed to be higher risk, and the firm struggles to find an insurer willing to offer Life Cover to those clients.

Heart conditions and circulatory conditions are among the most common health conditions we see in the clients referred to us by financial advisors.

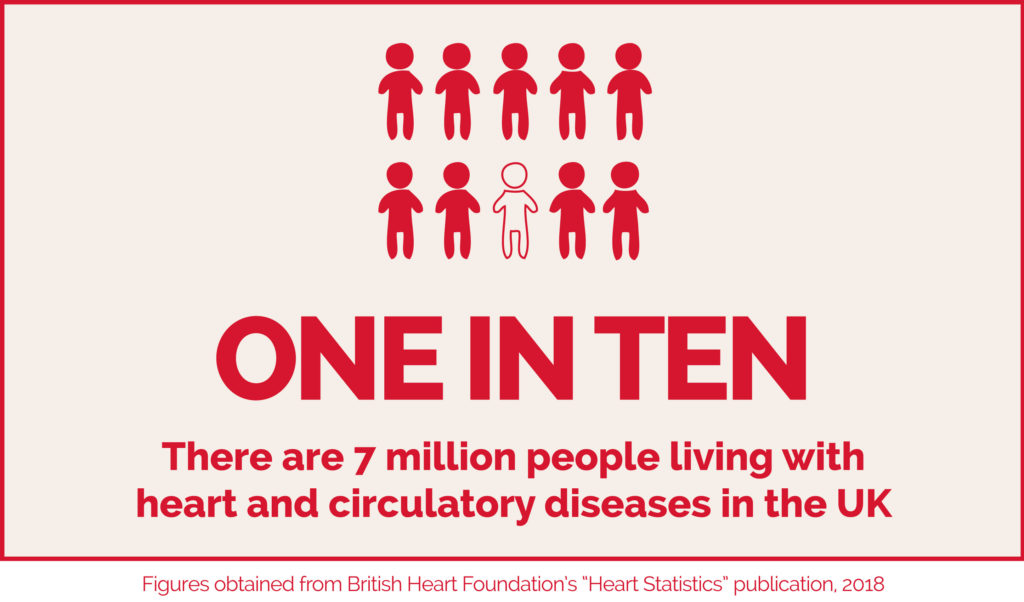

There are currently around 7 million people living with heart and circulatory diseases in the UK – that’s over 10 percent of the population[1]. An ageing and growing population and improved survival rates from heart and circulatory events (such as heart attack) could see this number increase in years to come. From conversations we have with clients, we know that many people wrongly assume that their heart condition automatically means they aren’t eligible to get any Life Insurance.

Around 80 percent of people with heart and circulatory diseases have at least one other health condition[1], which makes it even harder for these people to find an insurer willing to offer them Life Insurance, even with the help of their financial advisor.

Financial advisors don’t want to tell their clients they are uninsurable. This is why a growing number of financial advisor firms have an arrangement with specialist brokers like Moneysworth to handle their declined Life Insurance cases.

They care about their clients and realise they have a duty of care to help them find the insurance they need, even if that means referring the client to a specialist broker. This duty of care is the key reason why financial advisors should have contingency plans for signposting their clients to a specialist.

The financial advisors who come to us rely on our specialist expertise. Our careful research not only helps to ensure their client has the best chance of being offered cover, but quite often results in that cover being offered at a surprisingly affordable price.

Most important of all, our comprehensive approach also means the client can feel that the insurance cover they’ve purchased is fit for purpose so that – if the worst happens – the policy will pay out.

A financial advisor firm recently approached us having tried, unsuccessfully, to find Life Cover for their client who has a heart condition.

The client is a male in his early forties who was diagnosed with Cardiomyopathy over ten years ago. Cardiomyopathy is a disease of the heart muscle which affects its size, shape and structure.

At this time, he was also fitted with an ICD (Implantable Cardioverter Defibrillator) – a life-saving device which is surgically implanted inside a patient’s chest if their cardiologist believes there is a real risk that the heart could suddenly stop beating. An ICD is a defibrillator that automatically detects if the heart stops and immediately shocks the heart to start it beating again.

The client has annual medical reviews and, despite the seriousness of his heart condition, he has no symptoms whatsoever.

We were not surprised that the client and his financial advisor had experienced difficulty in finding an insurer willing to offer cover. We knew that the majority of Life Insurance companies will decline an application where an ICD had been fitted – especially given the underlying heart condition diagnosed at such a relatively young age.

When we completed our research for this case, virtually all insurers in the marketplace confirmed they would decline an application for Life Insurance. But because we were thorough, we found two insurance companies willing to give further consideration to an application, subject to seeing a GP report.

With the client’s permission, these two insurers obtained a GP report including a letter from the cardiologist.

One of these insurers then declined the application, but the other offered mortgage term assurance with no exclusions and for the full sum the client needed (over £200,000) for the whole term of the mortgage (over 20 years) for less than £100 per month.

A satisfying result for us, for the financial advisor and for their client!

Notes:

1. Figures obtained from British Heart Foundation’s “Heart Statistics” publication, 2018: https://www.bhf.org.uk/what-we-do/our-research/heart-statistics

This February is National Heart Month, a time for each of us to reflect on how we can improve the health of our heart. Living with a heart condition can affect not only the individual but their loved ones too.

Having a heart condition has become one of the most common medical problems among clients who ask us to help them find Life Cover.

Source: British Heart Foundation statistics

Finding Life Insurance that suits your needs can be much harder if you’ve had a heart attack, a cardiac arrest or are living with a heart condition. Moneysworth specialise in helping people find Life Cover even if they have a health condition or have been refused life cover elsewhere.

The most common heart condition we see in our work is a previous heart attack (also known as myocardial infarction). However, over the last seven months, we’ve helped over ninety people with a wide variety of other heart conditions to find life cover. Many of these clients have now successfully started their policy or are currently in the process of applying for cover.

Over the next few weeks, we’re going to post a series of articles about the circumstances behind some of our clients’ search for life cover: why they needed life insurance, the problems they’d previously encountered when trying to apply for cover elsewhere, and the policy options and prices we were able to obtain for them.

It may surprise you to see how people who are living with a serious heart condition – or even multiple conditions – are still able to find cover, thanks to our team’s expert guidance and assistance.

Whether you have diabetes or whether you are concerned about the possibility of being diagnosed with diabetes in the future you should take a minute to review your life cover. If you need more than its probably a good idea to act sooner rather than later.

Here’s why.

Currently Diabetic? – Once you have started your life cover, the terms (including the premium amounts) are generally guaranteed for the rest of the policy providing that continue to pay your premiums, irrespective of future changes in your health. Delaying taking out cover will generally end up costing you more money when you take out cover at a later date because you will be older. It may also cost you more because of the progress of your diabetes, especially if you develop more complications such as retinopathy, neuropathy or kidney issues. So again arranging your cover now protects you from the effects that future changes are likely to have if you delay. Worse still some future health developments could mean that it becomes impossible to be able to obtain life insurance. One highly relevant example of this would be the future development of any heart issues which is a significant additional risk factor for diabetics. Unfortunately no mainstream insurance companies will offer life cover to any diabetic, type 1 or type 2, who also then goes on to develop a condition such as angina or who has a heart attack. However the life insurance policy terms for those diabetics who arranged their life cover before they developed any heart conditions are still guaranteed, which also means that if death accours as a result of a heart attack you are still covered.

Not Currently Diabetic But Worried About Being Diagnosed With Diabetes In The Future?

You would also be well advised to review your life cover now rather than later. Now you may still be able to obatin life cover at lower premium rates and in the absence of any significant existing health factors there is a good chance that you may be able to so at ‘normal’ premium rates, which are the cheapest premium rates. Again if you take out the cover now these premium rates are generally guaranateed. If you delay sorting out your cover until you are diagnosed with diabetes, expect to pay higher premiums and in some cases much higher premium rates. Also if you delay until you are diagnosed you should expect to experience difficulty in being able to arrange some other valuable benefits, for example critical illness cover. This could mean for example if the purpose of the life insurance is pay off a mortgage that the option to include insurance to pay off the mortgage if you have a heart attack is simply no longer available to you even though the risk of it happening has increased.

How soon can someone apply for life insurance after suffering a heart attack?

This is a question we are often asked as we receive an increasing amount of enquiries from people who have suffered a heart attack (myocardial infarction). For those affected it is not surprising that their minds should turn to this subject. For having survived a heart attack we are normally given a little while to recover and for many this provides time to consider what the future might hold, especially for our familes and those who financially depend upon us.

For some it can be worrying to realise that they have insufficient life cover to repay the outstanding balance on the mortgage. This means that in the event of their death, amidst and that that would mean to their nearest and dearest, the family home may be at risk as well!

The mind then turns to questions about how difficult it might be to obtain life insurance following a heart attack and how long it might take to arrange for cover to be in place…………..

Well generally speaking the prospects are often better than might at first be assumed.

Firstly if you were over the age of 40 at the time of your heart attack and you have only had one heart attack there is a good chance that you will be able to obtain life insurance. However if your heart attack was severe or if you have further health conditions (eg diabetes) then you may find it difficult to obtain life cover.

Just how long it will take to obtain life cover after your heart attack will vary from one insurance company to another. Generally speaking most life insurance companies will be prepared to offer you cover twelve months after the heart attack and some will even consider offering terms six months.

It may even be possible to do even better than that! We know one or two life companies who may consider applications one month after the client suffering a heart attack, depending on the overall picture.

So if you, or someone you know, has recently suffered a heart attack, if you are worried that you have insufficient life cover in place to sufficiently protect your family, if you think its probably too late to get life cover……… don’t despair. It might be easier to get life cover than you think.